Reserve bank of australia

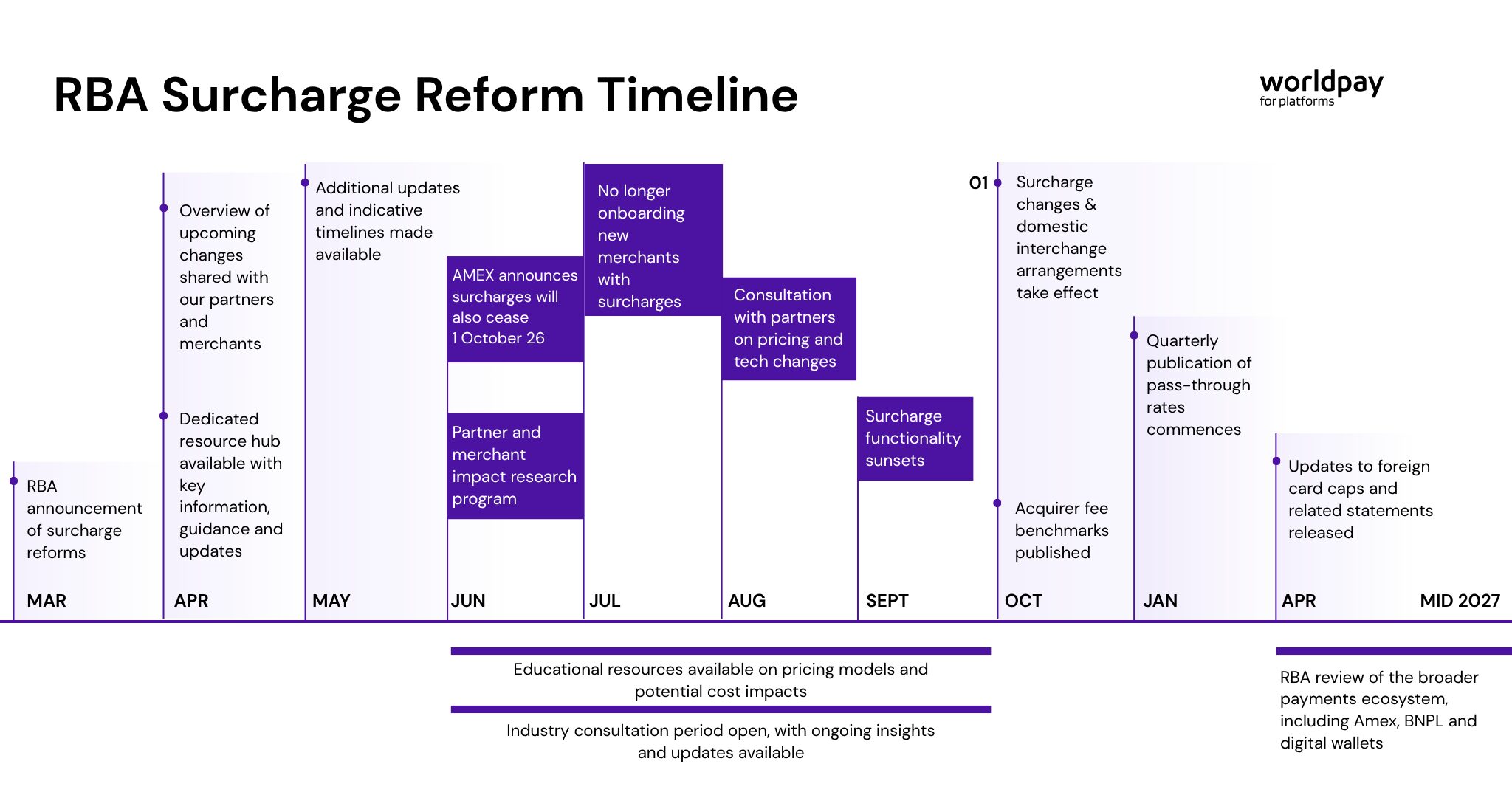

Australia's surcharge rules are changing.

Here's what that means for our software platforms and merchants.

Updated on 27 July 2026

From 1 October 2026, businesses in Australia will no longer be permitted to apply a surcharge to Visa, Mastercard, eftpos or American Express (Amex) card payments.

Whether you're a business accepting payments or a software partner supporting merchants, we're here to help you understand what is changing and prepare for the transition.

For merchants

Understand whether your business may be affected, what payment fees will continue to apply, and what you can do to prepare.

For software partners

Access approved messaging, FAQs and resources to support merchant conversations and prepare your business.

What is changing?

- From 1 October 2026, surcharges on Visa, Mastercard, eftpos and Amex card payments will no longer be permitted in Australia.

- Businesses will continue to incur payment processing costs when customers pay by card.

- The key change is that these costs can no longer be recovered through a separate card surcharge.

- This is an industry-wide transition. Changing payment providers will not alter the requirement.

Common questions

What is changing?

Do payment fees disappear?

Do I need to do anything now?

Where can I find information relevant to me?

Have further questions?

Our team will be available to answer any questions and walk through the implications for your specific business. If you have further questions before then, please contact us.